Traditional mortgage lenders want to see your W-2s, tax returns and personal income documentation — a process that creates challenges for self-employed investors and portfolio builders alike. When you write off business expenses or hold multiple rental properties, your tax returns often don’t reflect your true financial capacity. This rigid income verification slows your ability to acquire cash-flowing properties and scale your portfolio.

A debt service coverage ratio (DSCR) loan changes the equation. Instead of scrutinizing your personal income, lenders evaluate your property’s ability to cover its own debt.

DSCR Loans Explained

A DSCR loan is a mortgage designed for real estate investors, where lenders qualify borrowers based on their property’s cash flow instead of their personal income. Known as a non-QM or business-purpose loan, this financing solution evaluates whether rental income can cover the monthly mortgage payment. The lender focuses on the investment property’s performance, not on your traditional W-2 earnings or tax returns.

The DSCR approach has driven significant growth in the investor lending market, with DSCR loans representing roughly 30% of the non-QM sector as of 2025. For investors who struggle to document traditional income or whose tax strategies reduce their reported earnings, this financing method provides a clear path to property acquisition and portfolio expansion.

How to Calculate DSCR

The debt service coverage ratio is the central qualifying metric for these loans. Lenders use this to calculate whether your property generates enough income to cover your associated debt obligations. The formula divides the property’s net operating income by your total debt service, creating a ratio that reveals financial viability.

Understanding this calculation helps you evaluate potential acquisitions before approaching a lender.

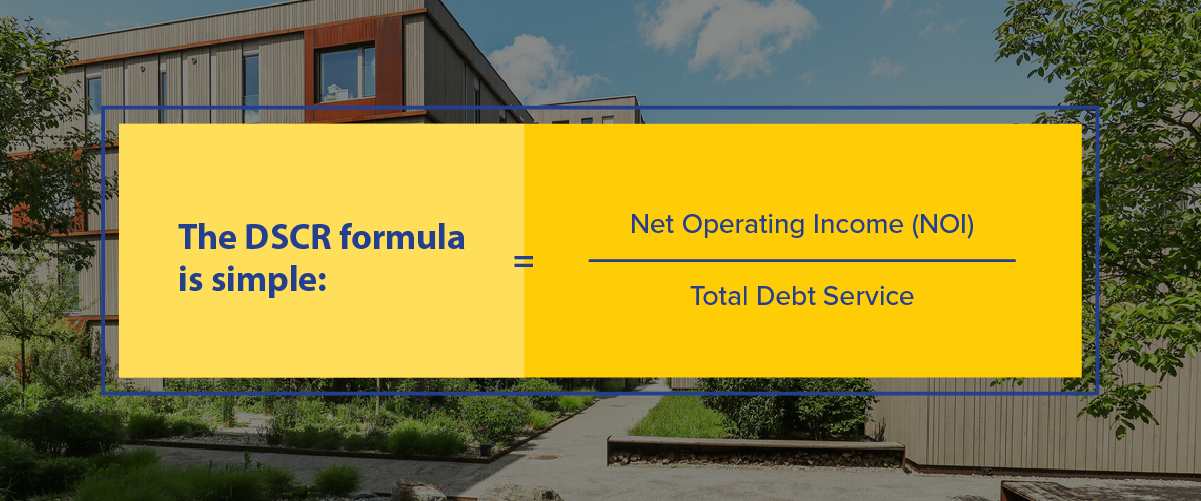

The DSCR Formula

The DSCR formula is simple: Net Operating Income (NOI) / Total Debt Service.

The NOI is the property’s income generated from operations after deducting all operating expenses, but before accounting for debt service, income taxes and depreciation.

For example, if your property earns you $3,000 in rent per month and the complete payment totals $2,400, your ratio calculates to 1.25. This demonstrates that the property produces 25% more income than is required to repay its debt. A ratio above 1.0 shows positive cash flow, while anything below signals the property doesn’t generate enough rent to support the loan.

You can estimate potential payments using a trustworthy mortgage calculator to test different scenarios and determine which of your properties meet lender thresholds.

What Is a Good DSCR Ratio?

DSCR ratios can be categorized as follows:

- Strong ratios: The best ratios typically fall between 1.20 and 1.50, demonstrating the property generates healthy cash flow beyond its obligations. A ratio above 1.25 positions you for the most favorable terms, as lenders view these deals as lower risk.

- Breakeven ratios: Properties at 1.0 represent breakeven performance — meaning the rent exactly covers the payment — and often serve as the minimum threshold lenders will accept.

- Negative ratios: Ratios below 1.0 indicate negative cash flow and require compensating strengths like substantial cash reserves or excellent credit.

The stronger your ratio, the easier it will be to secure more competitive pricing and terms.

Who Uses DSCR Loans?

Real estate investors turn to DSCR financing when conventional loans create obstacles to their portfolio growth. These loans serve specific investor profiles who face challenges with traditional income documentation or have outgrown the limits of standard financing products.

Self-Employed Investors

Business owners and self-employed professionals often write off significant expenses on their taxes, making their personal taxable income appear too low to qualify for conventional mortgages. Your actual cash flow may be substantial, but traditional lenders only see the reduced figure on your 1040.

DSCR loans solve this problem by ignoring personal tax documents entirely. The property’s rental income becomes the sole qualification factor, allowing you to leverage your investment expertise without penalty for smart tax planning. Some lenders offer specialized financing solutions for self-employed borrowers designed to work with your business structure rather than against it.

Investors With Multiple Properties

Fannie Mae caps conventional investment property financing at 10 mortgages per borrower, creating a hard ceiling for portfolio growth. Once you reach that limit, conventional financing becomes unavailable regardless of your financial strength or property performance.

DSCR loans remove this restriction entirely. You can scale beyond 10 properties and continue to acquire cash-flowing assets without arbitrary limits. This financing tool becomes essential for serious investors building portfolios of 15, 20 or 50+ rental units and who need consistent access to capital.

Investors Using an LLC

Holding property in a limited liability company shields your personal wealth from real estate risks. It creates a legal barrier between your rental business and your private assets, protecting you from liability claims related to tenant injuries or property issues.

Conventional loans typically don’t accommodate LLC ownership, forcing investors to hold properties in their personal names and sacrifice asset protection. DSCR loans are structured specifically for business entities, allowing you to maintain proper legal separation while accessing the financing you need to grow your portfolio.

DSCR vs. Conventional Loans

The differences between these two financing approaches highlight why DSCR loans serve investor needs more effectively:

- Income verification: DSCR loans qualify based on property cash flow, while conventional loans require W-2s, tax returns and employment verification.

- Property limits: DSCR financing allows unlimited properties. Conventional financing caps at 10 financed investment properties per borrower.

- Eligible borrowers: DSCR loans work for LLCs, self-employed investors and those with complex income structures. Conventional loans favor W-2 employees with straightforward income documentation.

- Down payment: DSCR loans typically require a 20%-25% down payment. Conventional loans may allow lower down payments depending on the property and borrower profile.

DSCR Loan Requirements

While requirements vary by lender and loan program, typical qualifications include:

- Credit score: Although there is no official guideline, most lenders require a minimum score, with better terms often available for higher scores.

- Down payment: Expect to put down 20%-25% of the purchase price.

- Cash reserves: Lenders typically want to see 3-12 months of mortgage payments in liquid reserves, depending on the loan size.

- Property type: Single-family homes, condos and multifamily properties generally qualify.

These are general guidelines rather than absolute rules. An experienced lender can provide specific details about their DSCR loan programs and help you understand which requirements apply to your situation.

Get a DSCR Loan With Pacific Mortgage Group

DSCR loans empower investors to grow their portfolios based on smart property acquisitions, not restrictive paperwork. Whether you’re self-employed, managing multiple properties or holding assets in an LLC, this financing solution removes the barriers that conventional lenders create. Pacific Mortgage Group understands the unique needs of real estate investors and guides clients through DSCR loan financing across California, Florida, Washington, Nevada, Oregon and Colorado.

Our experienced team provides personalized service and access to competitive wholesale lender rates, making the mortgage process efficient and transparent. To explore how a DSCR loan fits your investment strategy, connect with our loan team to review your property numbers and financing options.