If you are a first-time homebuyer in California, you can’t underestimate the importance of having competitive buying power. As of February 2026, the housing market does seem to be shifting in favor of buyers nationally, but the state’s astronomical house prices and intense competition between buyers remain.

Saving for a down payment is a tall order in California, and finding the right loan can help you secure your dream home with sustainable repayment terms.

This guide explores everything you need to know about Federal Housing Administration (FHA) loans and conventional loans, comparing costs, eligibility criteria and long-term strategies to help you decide which financing option is right for you.

Loan Basics for California Homebuyers

To decide which loan type is best for you, you need to understand the differences between FHA and conventional loans.

FHA Loans

FHA loans are government-backed mortgages designed to make buying property more accessible by lowering the barriers to property ownership. FHA loans are often a common choice for first-time home buyers since they are generally easier to qualify for than most conventional loans due to their:

- Lower credit score requirements

- Lower minimum down payments

- Lower closing costs

- Flexible debt-to-income ratios

An additional benefit of FHA loans for California residents is that the government adjusts its FHA borrowing limits annually, based on local median home prices and property location. This means that buyers looking to purchase homes in more expensive regions, such as San Francisco and Los Angeles, may be able to borrow above the standard national loan limit.

Conventional Loans

Conventional loans are not government-backed, but are instead offered by private lenders. Most conventional loans are designed to adhere to the uniform standards set by Fannie Mae and Freddie Mac.

Two of the most common conventional loans are:

- Conforming loans: The Federal Housing Finance Agency (FHFA) establishes lending limits, and its underwriting guidelines align with Fannie Mae and Freddie Mac.

- Nonconforming loans: These loans, which include jumbo loans, do not adhere to FHFA limits or the standardized Fannie Mae and Freddie Mac guidelines. Nonconforming loans may exceed standard lending limits but may be more difficult to qualify for and carry higher interest rates.

As many homes in California significantly exceed the average national home value, many buyers can benefit from the higher lending rates offered by nonconforming and jumbo loans.

However, unless you are planning to invest in property that exceeds the maximum conforming loan limits, first-time buyers may benefit more from the lower interest rates and stricter guidelines of conforming loans.

In today’s competitive market, conventional loans can signify a buyer’s financial strength, making their offer more appealing to sellers.

First-Time Buyer Status Benefits

The California Housing Finance Agency defines a first-time buyer as an individual who has not owned and lived in their own property — or lived in a home owned by their spouse — for the last three years.

Many California first-time homebuyers can benefit from state-specific assistance programs, many of which you can use in conjunction with specific first-time buyer loans.

First-time buyer assistance programs include:

- The Dream For All Shared Appreciation Loan: This program assists buyers with their down payment and must be used alongside California’s corresponding Dream For All conventional first mortgage. The program offers eligible buyers up to 20% of the down payment or closing costs, up to a maximum of $150,000.

- The CalHFA MyHome Assistance Program: This program offers a deferred secondary mortgage — or junior loan — for up to 3.5% of the home’s value. You can put this loan toward closing or down payment costs.

Key Qualification Factors Compared

When comparing your loan options, it’s important to understand their eligibility criteria.

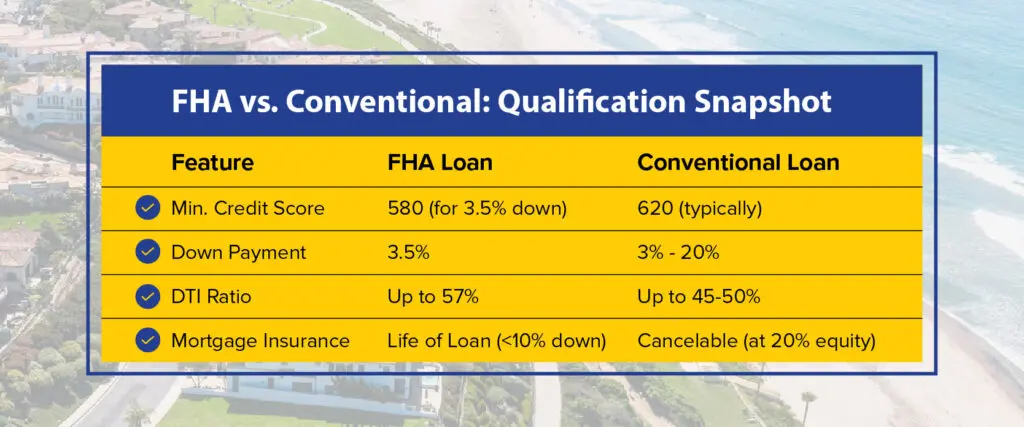

The qualifying criteria for an FHA loan in 2026 are:

- Credit score: You need a minimum credit score of 580 to qualify for a 3.5% down payment or a credit score of between 500 and 579 to qualify for a 10% down payment.

- Property requirements: The home you are borrowing money to finance must be your primary residence. The property’s standards must also be verified through an FHA appraisal.

- Minimum down payment: The minimum is 3.5%, provided your credit score is 580 or above. For example, for a $1 million property, you could qualify for a down payment of $35,000. Generally, FHA loans allow 100% of the down payment to come from gifted funds.

- Debt-to-income ratio: While some FHA-approved lenders require you to have a debt-to-income (DTI) ratio of 43% or less, other lenders may justify higher DTIs of up to 57% alongside strong compensating factors.

The qualifying criteria for a conventional loan in 2026 are:

- Credit score: Most lenders require a minimum score of 620, but a score of 700 or higher is often needed to secure competitive interest rates. Conventional interest rates can fluctuate depending on creditworthiness.

- Property requirements: The loan may be used for a primary, secondary or investment property. It must meet certain safety standards, but appraisals tend to be more lenient than for an FHA loan, making it ideal for buyers looking to buy to renovate.

- Minimum down payment: Most conventional down payment requirements begin at 3% for primary residences, but lenders may request up to 20% for standard borrowers.

- Debt-to-income ratio: The general maximum DTI is 45%, but lenders may go up to 50% for extremely strong applications.

Cost Comparison in California

California’s many regions offer different loan limits and mortgage insurance rates.

California Loan Limits by Region

All California regions have their own floor and ceiling limits, which establish the minimum and maximum loan amounts and interest rates, and protect the lender and borrower, respectively.

For example, here are the FHA loan limits for one-unit properties in different locations:

- LA and Orange County: The ceiling limit is $1,249,125.

- Riverside and San Bernardino: The ceiling limit is $690,000.

Mortgage Insurance Comparison: PMI vs. MIP

FHA loans require buyers to pay two types of mortgage insurance premiums (MIPs) — an up front MIP and an annual MIP, which buyers pay monthly. For buyers who make a down payment of less than 10% of the property value, their MIP remains for the life of the loan.

Conversely, conventional loans do not require MIPs. Instead, buyers must pay private mortgage insurance (PMI) if their down payment is less than 20% of the property value. Whereas MIPs remain valid for life, PMI typically ends automatically when the home reaches 78% loan-to-value, or you can cancel it at 80%. These terms can provide first-time buyers with a more flexible long-term exit strategy that FHA loans lack.

Total Cost Analysis

FHA loans often appeal to first-time buyers due to their lower interest rates and initial monthly payments. However, these government-backed loans often incur higher long-term costs than conventional loans with their permanent MIP payment requirements.

To understand which loan type best suits your needs, you should explore the annual percentage rate (APR) of each specific loan.

Decision Framework for California Buyers

Discover which framework suits your needs.

When to Choose an FHA in California

As a first-time buyer, you should consider choosing an FHA if:

- Your credit score is below 680.

- Your DTI ratio is higher than 43%.

- You are buying a multiunit property with between two and four units.

- You are happy to buy now, build equity and refinance to more beneficial conventional loan terms in the future.

When to Choose a Conventional Loan in California

You should choose the conventional route if:

- Your credit score is 720 or above.

- You can afford a higher down payment of 10%-20% to minimize your PMI.

- You would prefer a lower lifetime cost and no up front fees.

Find Your Best Solution With Pacific Mortgage Group

While both FHA and conventional loans are viable pathways for building your wealth in California, choosing a solution that’s right for you depends on your unique financial situation and preferences.

At Pacific Mortgage Group, we provide personalized evaluations to ensure every client achieves their home ownership goals while keeping their best interests in mind. With digital application options and a variety of solutions on offer, our services keep up with California’s fast-moving housing market and help buyers retain a competitive edge.

To find out more about our custom rates, contact Pacific Mortgage Group for a quote today.